China-Europe Rail Freight 2026: Impact on Road Transport

China-Europe rail freight 2026 surged 25% to 352,100 TEU. See how the intermodal boom is reshaping Polish, German, and Benelux road freight demand.

Logifie Team

Logistics Technology Experts

The 352,100 TEU moved on the China-Europe Railway Express in January and February 2026 is not only a rail milestone. It is also a truck-demand shock for terminals, customs brokers, and last-mile carriers across Poland, Germany, Benelux, and Central Europe.

China-Europe Rail Freight 2026: Impact on Road Transport

The china europe rail freight 2026 story is larger than a modal-shift headline. RailFreight.com reported a 25.2% year-on-year rise in TEU, but every container that reaches a European terminal still needs a truck for customs delivery, cross-dock transfer, or final-mile distribution.

For carriers and shippers using real-time visibility on cross-border lanes, the operational question is no longer whether rail matters. It is how quickly your network can react when 3,501 train trips push more boxes into Malaszewicze, Duisburg, and Budapest within tighter delivery windows.

352,100 TEU

China-Europe rail freight volumes rose 25.2% year on year in the first two months of 2026.

What Happened on the China-Europe Corridor

On March 19, 2026, a Chengdu-to-Poland service marked the 120,000th cumulative China-Europe trip , a milestone that also pushed the network's total cargo value above $490 billion. That milestone matters because it confirms the corridor is now a permanent part of European import planning, not a niche overflow channel.

The acceleration in early 2026 was even more important. anewz.tv counted 3,501 train trips in January and February alone, up 31.7% from the same period in 2025. The trip count grew faster than TEU, signaling more frequent departures and denser terminal activity on the European side.

The growth was not evenly distributed. Outbound China-to-Europe trips jumped to 1,736 and carried 181,200 TEU, while inbound European-origin services rose more moderately. Caixin Global linked the pattern to shifting supply chains and a 12% increase in China-Russia trade, which reinforces pressure on western terminal gateways.

The route map is also widening. 128 Chinese cities now connect to 232 European cities across 26 countries, which means more inland hubs can feed cross-border truck networks instead of relying only on seaports.

The big operational risk is the imbalance between outbound and inbound growth. More import-heavy rail flows into the EU create asymmetric terminal congestion and tighter truck scheduling around unloading, customs, and final-mile dispatch.

By the Numbers: Why Rail Is Winning Urgent Cargo

Rail is benefiting from a rare combination of speed, resilience, and narrowing cost gaps. With maritime routes still disrupted and air freight too expensive for many categories, the Eurasian land bridge looks commercially credible for shippers that need faster replenishment without paying premium air rates.

3,501

Trip frequency rose 31.7% year on year, giving importers more departure options and European terminals more arrivals to process.

+47.5%

China-to-Europe departures expanded much faster than inbound services, which concentrates delivery pressure on EU road networks.

| Metric | Jan-Feb 2025 | Jan-Feb 2026 | Change |

|---|---|---|---|

| Total train trips | 2,658 | 3,501 | +31.7% |

| Total TEU moved | 281,200 | 352,100 | +25.2% |

| Outbound trips (China to Europe) | 1,176 | 1,736 | +47.5% |

| Outbound TEU | 128,500 | 181,200 | +41.0% |

| Inbound trips (Europe to China) | 1,482 | 1,765 | +19.2% |

| Inbound TEU | 152,700 | 170,900 | +11.9% |

| European cities served | ~220 | 232 | +12 cities |

Those figures matter because they change the rhythm of road operations. Higher train frequency means more container batches arriving inside narrow pickup windows, while higher outbound TEU density increases the need for pre-booked truck capacity, customs coordination, and short-term warehousing around terminal hubs.

Why the Rail Surge Matters to European Road Freight

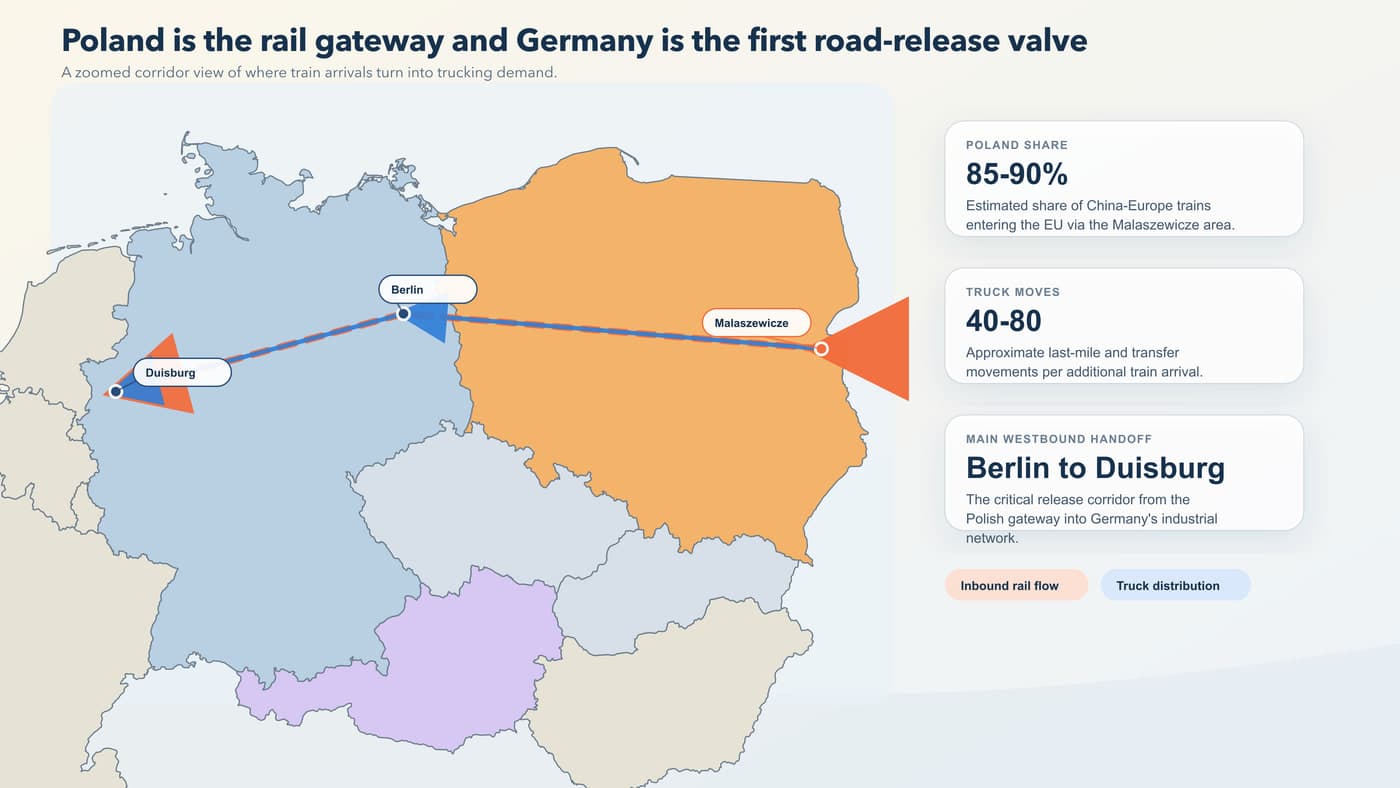

The most important gateway is still Malaszewicze in Poland , where an estimated 85-90% of China-Europe trains enter the EU. That makes eastern Poland one of the most important truck-demand concentration points in the entire European logistics network.

At that border gateway, containers move from 1,520 mm broad gauge to 1,435 mm European gauge or directly onto trucks. Each extra train creates more work for drayage, final-mile, bonded storage, and customs-cleared road distribution across Poland and Germany.

"When long-haul road costs rise, intermodal becomes more attractive, but the truck remains indispensable on the first and last mile."

- UIRR market insight, 2026

That quote fits the 2026 cost backdrop. UIRR-linked reporting highlighted Austrian tolls up 7.7%, Flanders charges up 20%, and the Netherlands moving toward distance-based charging. Those changes weaken pure long-haul road economics but raise the value of short, time-critical terminal trucking.

The policy backdrop reinforces the same trend. New EU multimodal aid rules take effect on March 30, 2026 and lift modal-shift aid ceilings from 50% to 90%, giving forwarders and logistics companies even more reason to shift trunk-haul volume to rail while buying road capacity around terminal nodes.

85-90%

Most China-Europe trains still cross into the EU through Malaszewicze, turning Poland into the main road-distribution springboard.

- Poland-Germany corridor - the A2 and A4 motorway spine becomes more valuable as terminal throughput rises in eastern Poland.

- Germany-Benelux corridor - Duisburg remains the western redistribution hub for rail-borne imports headed to the Netherlands, Belgium, and northern France.

- Budapest-Vienna-Milan corridor - southern terminal growth creates new demand for cross-border trucking into Austria and northern Italy.

- Terminal services layer - customs brokerage, bonded warehousing, and short-haul LTL distribution all expand when rail volumes bunch into predictable arrival waves.

Carriers located within a two-to-four-hour radius of Malaszewicze, Duisburg, or Budapest are no longer selling only capacity. They are selling terminal responsiveness and the ability to absorb schedule volatility without missed delivery slots.

Rail vs Ocean vs Road: The 2026 Corridor Economics

Mode choice is shifting because the old rail premium is less decisive. Dimerco's 13-25 day rail estimate looks far more compelling when ocean routings stretch to 35-50 days because of Suez and Hormuz disruption, and when emergency fuel surcharges squeeze sea economics.

| Factor | Ocean (via Suez or Cape) | Rail (via Eurasian corridors) | Road (terminal leg only) |

|---|---|---|---|

| Transit time | 35-50 days | 13-25 days | 1-5 days |

| Indicative cost per TEU | $2,500-$4,700 | $1,500-$5,500 | EUR 800-EUR 2,500 |

| Current reliability | Disrupted by diversions | More stable overland | Depends on driver and slot availability |

| Best use case | Lowest urgency freight | Time-sensitive replenishment | Final delivery and terminal drayage |

| Operational implication | Longer inventory exposure | Higher terminal intensity in Europe | More value in flexible local capacity |

Road still wins on agility after terminal arrival. That is why shippers increasingly need a mix of FTL, LTL, and customs-ready visibility supported by tools like Logifie quote workflows and fuel monitoring when pricing the last leg.

13-25 days

Rail currently offers a much faster Asia-Europe transit window than ocean while staying far cheaper than air freight.

What Shippers and Carriers Should Do Now

The 2026 surge should be treated as a network-design signal, not as a temporary news item. Shippers that map terminal exposure early and carriers that align fleets with intermodal handoff points will be better placed when Q2 and Q3 peaks add more volatility to already busy corridors.

- Map terminal proximity - measure how close your depots and partner fleets are to Malaszewicze, Duisburg, Budapest, and secondary inland terminals.

- Secure dispatch visibility - use tracking and ETA workflows so truck capacity is aligned with train arrival patterns rather than static weekly assumptions.

- Reprice corridor legs - update rates on Poland-Germany and Germany-Benelux lanes to reflect tighter pickup windows, toll inflation, and terminal waiting risk.

- Prepare LTL options - consolidate lower-volume terminal freight so intermodal arrivals do not force empty or underutilized FTL departures.

- Watch fuel and holiday calendars - combine fuel price monitoring with cross-border holiday planning before quoting terminal-driven road legs.

- Plan customs and compliance - intermodal speed loses value quickly if ICS2, transit, and proof-of-delivery steps are not synchronized across rail and road partners.

If your pricing model still assumes road-only competition on Asia-linked lanes, you are missing the fact that terminal-driven road demand is already changing lane economics in Poland and Germany first, and it will spread west as volume keeps compounding.

FAQ

How much has China-Europe rail freight grown in 2026?

In January and February 2026, the corridor moved 352,100 TEU across 3,501 train trips, according to RailFreight.com and anewz.tv . That equals a 25.2% rise in TEU and a 31.7% rise in trips versus the same period in 2025.

What is driving the shift from ocean to rail freight on China-Europe routes?

Three forces are converging: maritime disruption in the Red Sea and Hormuz area, faster 13-25 day rail transit, and a narrower cost gap as ocean carriers add surcharges and diversions. For shippers that need inventory back in Europe quickly, rail now offers a middle ground between slow sea freight and costly air cargo.

How does the China-Europe rail surge affect European road freight operators?

It creates more work around terminal distribution, customs handoff, and short-haul cross-border trucking. Because most trains enter through Poland and then flow toward Germany and Benelux, the road winners are carriers that can offer fast terminal response and reliable ETA control rather than only long-haul linehaul capacity.

Conclusion: Rail Growth Is Creating More Road Work, Not Less

The headline number in china europe rail freight 2026 is the 25.2% surge in TEU, but the commercial takeaway for Europe is simpler: faster rail growth means more terminal-driven trucking, more corridor repricing, and more value in cross-border operational control. The companies that treat rail as a source of new road demand - not as a threat to road demand - will be better positioned for the rest of 2026.

If you need more lane-level context, Logifie's market analysis and about page explain how cross-border visibility, carrier coordination, and pricing intelligence fit together when intermodal volumes accelerate.

Sources

China-Europe rail freight surged 25.2% year on year to 352,100 TEU in January and February 2026, with strong outbound growth from China to Europe.

The corridor handled 3,501 train trips in the first two months of 2026, up 31.7% from a year earlier.

China-Europe Railway Express passed the 120,000-trip milestone and now connects 128 Chinese cities with 232 European cities across 26 countries.

Malaszewicze handles an estimated 85-90% of China-Europe trains entering the EU and is expanding its multimodal capacity.

Rail transit from China to Europe typically runs 13-25 days, preserving a major speed advantage over ocean freight.

Road cost inflation and intermodal competitiveness signals remain visible in 2026 as tolls and access charges rise across key European markets.