EU Multimodal Freight State Aid 2026: Road Freight Impact

EU multimodal freight state aid 2026 lifts rail and intermodal aid to 90%. See which road corridors, carriers, and shippers face the biggest impact.

Logifie Team

Logistics Technology Experts

The European Commission's March 16, 2026 package lets Member States support qualifying rail and multimodal freight projects at up to 90% of eligible costs from March 30 onward, sharply changing the policy backdrop for long-haul road freight.

EU Multimodal Freight State Aid 2026: Road Freight Impact

The new EU multimodal freight state aid 2026 framework lands at a moment when road still carries 78% of inland EU freight. That is why the March 30, 2026 effective date matters: Brussels is no longer relying on slow policy nudges, but on direct financial acceleration for rail, inland waterway, and intermodal projects.

For road carriers, shippers, and freight forwarders, the immediate question is not whether trucks disappear. It is which corridors, cost models, and lane strategies become more exposed once governments can fund terminals, sidings, and modal-shift services without months of prior notification. The practical pressure will be selective and corridor-led, but it starts with planning now.

90%

Member States can now cover up to 90% of eligible multimodal and rail project costs under the new framework.

What Happened: March 16 Adopted Rules, March 30 Effective Date

On March 16, 2026, the European Commission formally adopted the Land and Multimodal Transport Guidelines and the Transport Block Exemption Regulation, replacing state-aid rules that had framed rail support since 2008. The new package takes effect on March 30, 2026, while the TBER remains valid through December 31, 2034.

The old regime was narrow and capped: it mainly targeted railway undertakings and limited support to 50% of eligible costs. RailFreight.com reported that the new framework nearly doubles the ceiling and broadens access to logistics companies, freight forwarders, multimodal transport operators, shunting companies, and vehicle owners choosing rail over road.

The TBER is the most operationally disruptive part because it removes the need for prior individual notification for a wide set of rail, inland waterway, and multimodal measures. trans.info summarized the result clearly: governments can move on terminals, sidings, new connections, and handling equipment much faster than before.

That matters most on first- and last-mile road legs attached to intermodal systems. The Commission itself highlighted private sidings as a way to reduce dependence on short feeder truck moves, making the change feel far more commercial than theoretical for road operators concentrated around rail-served industrial zones.

The key policy change is not only the 90% subsidy ceiling. It is the fact that qualifying projects can now move with far less administrative drag, compressing the response window for long-haul road networks.

By the Numbers: What Brussels Is Trying to Change

The modal-split picture shows why Brussels chose a finance-led intervention rather than another round of soft guidance. Road continues to dominate inland freight, while rail remains well below the bloc's long-term ambitions despite years of policy support and green-transition rhetoric.

78%

Eurostat data for 2023 shows road still dominates inland tonne-kilometres across the EU.

50%

The old 2008 state-aid framework limited support to half of eligible project costs.

2034

The new block exemption remains in force through December 31, 2034, giving the market a long planning runway.

| Metric | Figure | Source |

|---|---|---|

| EU road freight market share (inland, 2023) | 78% of tonne-km | Eurostat |

| EU rail freight market share (inland, 2023) | 17% of tonne-km | Eurostat |

| EU road freight volume (2024) | 1,867 billion tonne-km | Eurostat |

| EU target for rail freight by 2030 | 30% modal share | EU Green Deal |

| Previous maximum rail aid | 50% of eligible costs | EC 2008 guidelines |

| New rail and multimodal aid ceiling | 90% of eligible costs | EC LMTG 2026 |

| Annual rail infrastructure investment need | EUR 16.5 billion | European investment analysis |

| Annual intermodal facility investment need | EUR 1.5 billion | European investment analysis |

| TBER validity period | Until 31 Dec 2034 | European Commission |

Eurostat's modal split data shows that road gained share over the last decade while rail slipped back. That makes the new package Brussels' strongest attempt yet to buy faster modal shift with state-backed capital deployment rather than waiting for pure market forces to solve the gap.

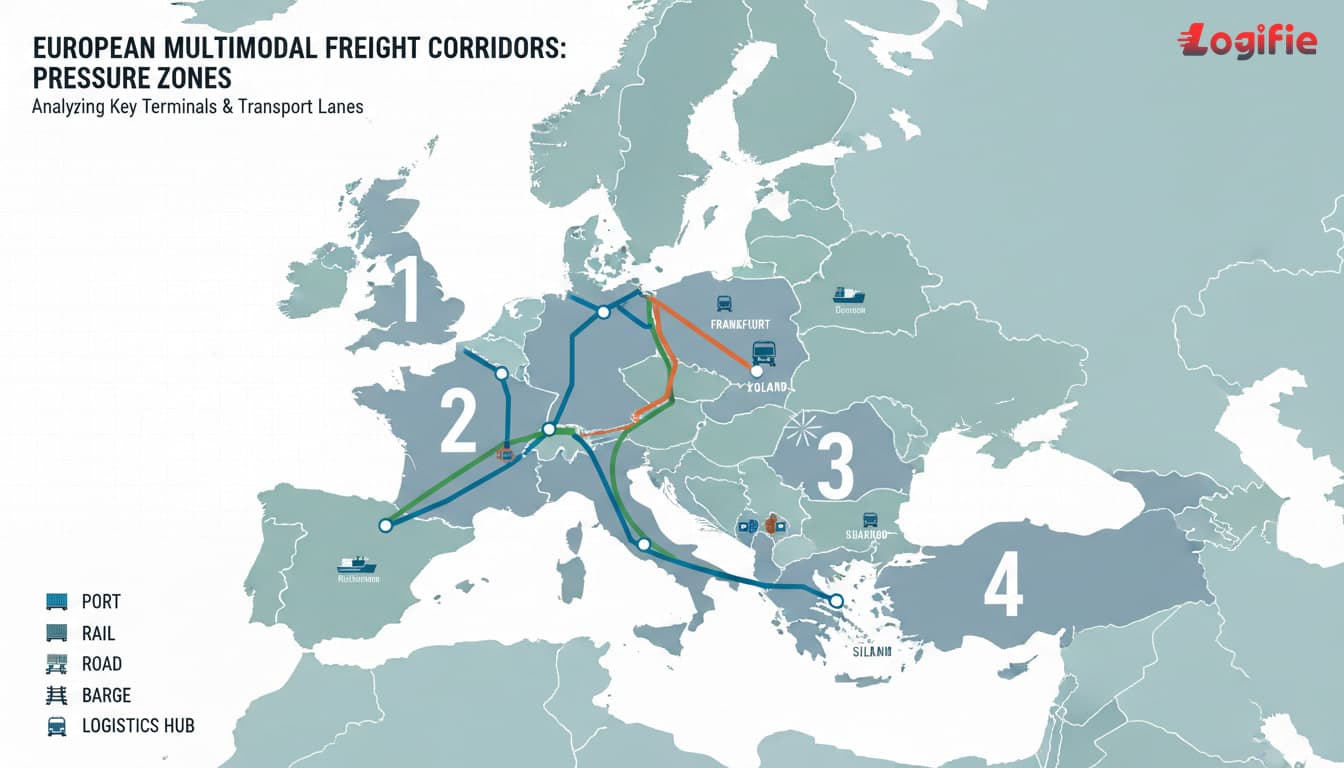

Which Corridors Face the Greatest Modal Shift Pressure

Not every road lane is exposed in the same way. Intermodal economics work best where distance, terminal access, and subsidy-backed infrastructure combine into a credible service alternative. The biggest risk sits on trunk corridors where governments can use the new framework to speed up projects that were previously too slow or too expensive to scale.

Germany-Italy via Brenner

The Brenner axis is already one of Europe's most watched modal shift battlegrounds because high cross-border volumes, Alpine constraints, and established combined-transport patterns give subsidies a fast route into the market. If Austria and Germany speed up terminal or siding support, long-haul road operators on this lane face earlier price pressure than most other corridors.

Germany-Spain and Germany-France

These long trunk routes sit in the 1,200-1,600 km range where combined road-rail models become commercially meaningful once infrastructure support improves. Faster funding for terminals, track interfaces, and handling equipment can turn what used to be marginal intermodal concepts into real procurement options for shippers with regular volumes.

Poland-Germany-Benelux

The Poland-Germany-Western Europe axis is the most important volume story because Poland alone generates 20% of EU road freight tonne-km . Any subsidised ramp-up in intermodal handling across this corridor would not replace trucking overnight, but it could shift tender dynamics, linehaul pricing, and capacity planning in the bloc's highest-volume overland market.

Rhine and Danube Waterway Corridors

The new rules also cover inland waterway freight, which matters because barge-linked networks can displace both trunk trucking and feeder road moves when public support improves terminal and connection quality. For road carriers around Rotterdam, Cologne, Basel, Vienna, Bratislava, Budapest, and Romanian Danube nodes, that creates selective competition at the edges of their current service mix.

The highest-risk corridors combine long distance, dense volumes, and strong terminal ecosystems. Where those three factors line up, the new state-aid rules can change tenders faster than carriers expect.

What the TBER Fast Track Means for Road Freight Competition

"Private sidings play a key role in reducing the need for first- and last-mile road transport for freight."

- European Commission

Before the TBER, a Member State often had to prepare a notification file and wait for Brussels to approve support above certain thresholds. That process acted as a bureaucratic brake on intermodal investment. The new block exemption removes much of that friction, letting governments approve qualifying measures with commercially useful speed.

That matters because road transport already runs on an efficient private asset base of trucks, depots, trailers, and dispatch capacity. Rail and barge systems need coordinated infrastructure spending, so the practical competitive effect of the new rules is to de-risk those investments for both governments and terminal operators. Aid for new services can also last up to five years, which is long enough to test routes that previously lacked private backing.

For road carriers, the biggest near-term exposure sits in the 300-1,000 km band where linehaul economics are already close enough for intermodal to compete if infrastructure costs fall. That is why operators should treat the reform as a lane-level pricing issue, not just a policy story.

- Terminal projects can now reach market faster, changing shipper procurement timelines.

- Private sidings and handling equipment can weaken short feeder truck demand around rail-served industrial sites.

- Service subsidies up to five years let governments prove new multimodal lanes before full commercial maturity.

Cost Implications for Shippers and Logistics Managers

For shippers, the most important implication is that the new rules create a planning dynamic rather than an instant cost reset. Intermodal alternatives still need time to become operational, but once funding decisions begin, procurement teams on long lanes will see more credible alternatives in tenders and budget scenarios.

- Potential upside is stronger intermodal price competition on long trunk lanes such as Germany-Spain, Germany-Italy, and Poland-Western Europe.

- Near-term reality is that road remains dominant because the EU is still far from its 30% rail-freight target and infrastructure delivery takes years.

- Transit-time trade-off keeps road attractive for time-critical freight, just-in-time production, and loads that depend on real-time shipment visibility across borders.

- Carbon reporting pressure will push some shippers to pilot lower-emission modes sooner as CSRD and Scope 3 reporting expectations tighten.

That means budget planning should combine lane economics, service level, and fuel cost visibility. Teams comparing road and intermodal scenarios should track real diesel inputs through Logifie's fuel price hub and test which corridors could realistically absorb more rail or barge share over the next two to five years.

EUR 16.5B

Industry analysis suggests Europe still needs EUR 16.5 billion per year in rail infrastructure investment to meet modal-shift goals.

The most pragmatic shipper response is to treat the reform as a corridor-screening exercise, piloting intermodal only where service reliability, CO2 gains, and total landed cost justify the shift.

What Road Carriers Should Do Right Now

The new framework does not create instant disruption, but it does create a multi-year strategic headwind for operators concentrated on long-haul FTL corridors. The right response is to sharpen pricing, lane monitoring, and service differentiation before subsidy-backed alternatives become embedded in tenders.

- Map corridor exposure by identifying lanes above 500 km with strong terminal density and cross-border volumes.

- Monitor Member State implementation from April 2026 onward, especially in Germany, France, Poland, Spain, Italy, Austria, and Benelux markets.

- Differentiate on speed and flexibility where road still outperforms rail on booking agility, door-to-door transit time, and recovery from disruption.

- Reprice long-haul lanes early before intermodal pilots reset procurement expectations on your largest corridors.

- Offer first- and last-mile partnerships because intermodal growth still relies on road execution around terminals and sidings.

- Improve ETA transparency with customer-facing tracking that highlights road freight's operational advantage.

- Bring carbon data into sales conversations so shippers compare total supply-chain performance rather than emissions in isolation.

- Use calendar risk planning by checking public holiday disruptions that can damage multimodal timetable reliability.

- Diversify beyond long-haul FTL only if your portfolio is heavily concentrated on corridors that fit intermodal economics.

- Review subsidy eligibility if your business already touches rail, barge, shunting, or terminal-linked services that could qualify under the wider rules.

FAQ

What is the EU Land and Multimodal Transport Guidelines (LMTG)?

The LMTG is the Commission's new state-aid framework for rail, inland waterways, and multimodal freight. Adopted on March 16, 2026, it replaces the 2008 rules and raises aid intensity to up to 90% of eligible costs while extending eligibility beyond railway undertakings to logistics and transport operators choosing non-road modes.

How does EU state aid affect road freight carriers in 2026?

It does not regulate road carriers directly, but it changes the competitive environment by making intermodal and waterway projects easier to fund and faster to launch. The effect is likely to be gradual rather than immediate, with the strongest pressure on long-haul trunk corridors above roughly 500 km.

Will EU rail subsidies reduce trucking demand in Europe?

Not dramatically in the short term because road still handles 78% of inland EU freight and the infrastructure gap remains large. The realistic scenario is selective modal shift on the strongest corridors, not a sudden collapse in truck volumes across the wider European market.

Conclusion

The new EU multimodal freight state aid package is a structural shift in how Europe will try to rebalance freight away from road. By combining a 90% aid ceiling with a faster approval route, Brussels has created tools that are materially stronger than the framework operators have worked under since 2008.

Road freight will remain dominant for years, but carriers and shippers that monitor corridor exposure, protect service quality, and keep up with market intelligence will be better positioned than those who treat the March 30, 2026 start date as just another Brussels headline.

New EU state aid guidelines increase coverage to 90%

Commission adopts new State aid rules to boost the use of more sustainable ways of transport

EU clears way for quicker funding of multimodal freight

Freight transport statistics - modal split

EU road freight transport sees 0.6% increase in 2024

Europe Road Freight Transportation Market Size

European investment in the rail freight market and intermodality