EU-US Trade War 2026: How Retaliatory Tariffs Are Reshaping European Road Freight

EU retaliatory tariffs start April 1, 2026. See how the EU-US trade war is lifting freight rates, filling warehouses, and pressuring European shippers.

Logifie Team

Logistics Technology Experts

Brussels has confirmed €26 billion in retaliatory tariffs on US goods, with Phase 1 effective April 1, 2026, turning trade policy into an immediate road freight planning problem.

EU-US Trade War 2026: How Retaliatory Tariffs Are Reshaping European Road Freight

European shippers had 11 days to react after the European Commission set an April 1, 2026 start date for retaliatory duties covering €26 billion of US goods. The EU-US trade war is no longer a distant policy debate: it is already distorting road capacity, warehouse availability, and customs planning across Europe's export corridors.

€26B

Phase 1 retaliatory tariffs on US goods start on April 1, 2026, forcing immediate freight planning changes.

What Happened: From Trade Deal Tension to April 1 Tariff Shock

The current escalation started after Washington raised duties on steel and aluminium derivatives to 50%, far above the earlier baseline embedded in the 2025 trade understanding. CNBC reported that the European Parliament suspended progress on ratifying the deal once those higher duties hit derivative product categories.

On March 11, the EU answered with a two-phase retaliation plan covering US exports worth roughly the same magnitude. White & Case confirmed that consumer goods, agricultural goods, and industrial items are in the first wave, giving shippers only a short window to accelerate arrivals before the deadline.

At the same time, French officials have pushed the bloc to consider the Anti-Coercion Instrument if Washington keeps escalating. That matters for road operators because a broader dispute would not just change import prices; it could redirect entire lane structures across European ports, bonded warehouses, and inland depots.

April 1 is a customs cutoff, not just a political milestone. Loads arriving after the date may face new duty treatment, origin checks, and clearance delays even if they were booked weeks earlier.

By the Numbers: The Freight Pressure Is Already Visible

The most useful signal is not the headline politics but the operational data already showing frontloading, inland haul acceleration, and a warehouse squeeze across European gateways.

+22.4%

Year-on-year growth in February 2026 as exporters rushed cargo out before the next tariff step.

57%

Top European shippers accelerated inland freight to beat tariff deadlines and secure port slots.

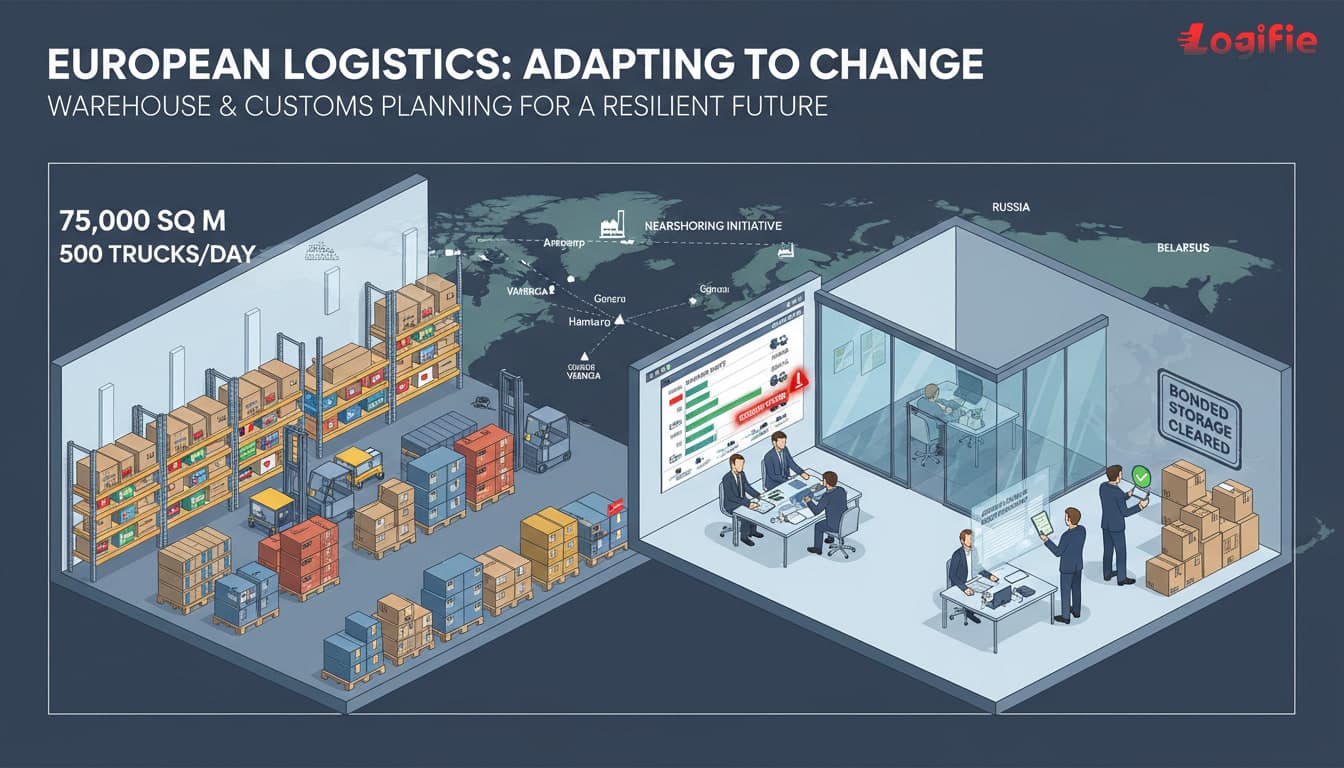

<5%

Europe's top 30 logistics markets are effectively full, tightening bonded warehouse and overflow storage options.

| Metric | Figure | Source |

|---|---|---|

| EU exports to the US, February 2026 YoY | +22.4% | Eurostat / Scangl |

| European shippers expediting inland hauls | 57% | Scangl / AlixPartners |

| US goods covered by EU countermeasures | €26 billion | EU Commission / White & Case |

| US tariff on EU steel and aluminium derivatives | 50% | CNBC |

| Vacancy rate at top 30 European logistics markets | <5% | AlixPartners |

| IRU road freight contract index | 128.9 | IRU / GetTransport |

| Contracted European road freight rate forecast for 2026 | +3% YoY | transportmanagement.org |

Taken together, these figures show a market that is already in pre-deadline compression: more export freight moving fast, less storage slack available, and a growing risk that shippers will pay for panic capacity in late March and early April.

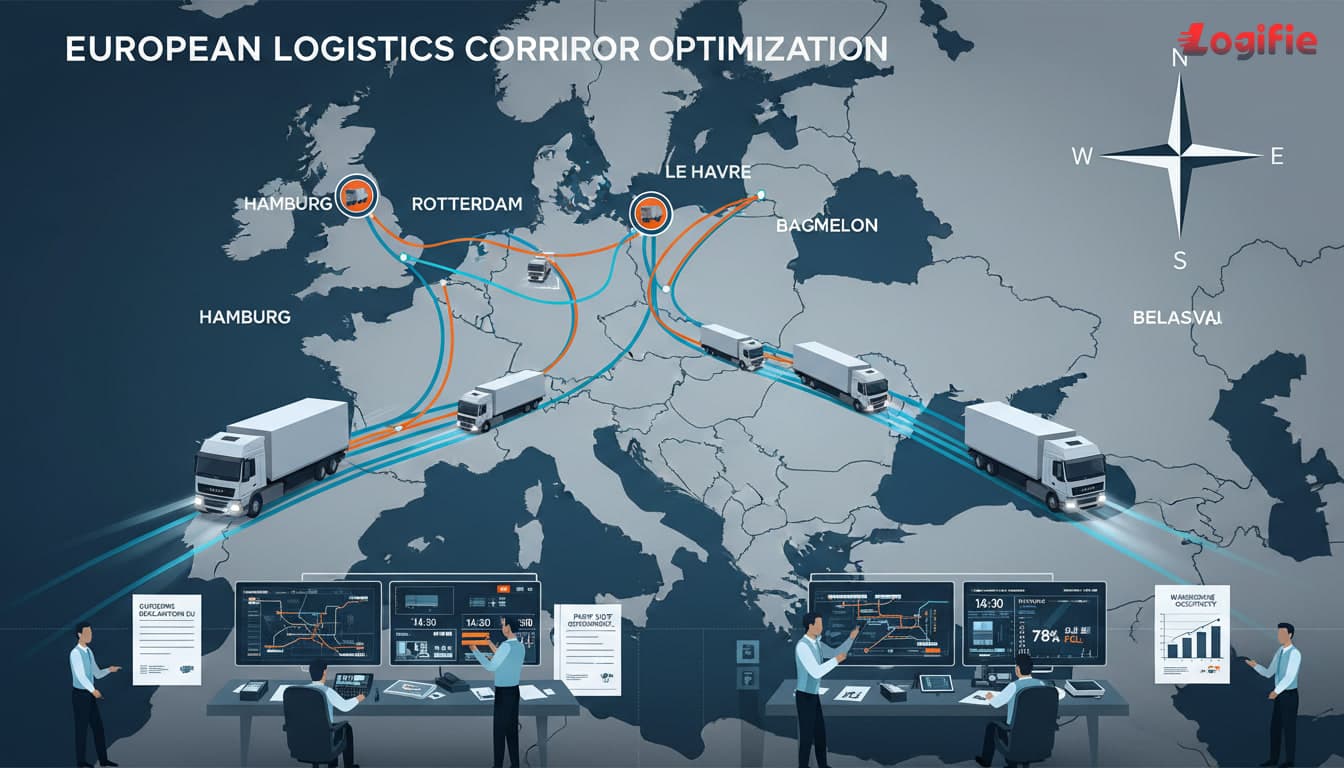

How EU Road Freight Corridors Are Already Under Stress

The surge is hitting corridors where FTL export flows and LTL feeder moves converge on Atlantic gateways. That mix creates uneven pressure: some lanes fill with urgent export freight while adjacent lanes lose flexibility for repositioning empties and weekend recovery moves.

The Germany-Hamburg axis is the clearest example. Automotive, machinery, and chemicals exporters are accelerating domestic drayage and long-haul feeder work toward northern ports, and the resulting inland squeeze is already showing up in lane planning discussions across German contract fleets.

The Rhine-Rotterdam corridor faces a double hit from trade-war frontloading and warehouse scarcity. As bonded storage tightens, importers are forced to use overflow facilities farther inland, which pushes more short-notice shuttle work onto truck operators and stretches yard-to-warehouse cycles well beyond normal turn times.

France to Le Havre and Spain to Barcelona are also under pressure as food, consumer goods, and industrial exporters attempt to frontload before the first EU countermeasures land. That is increasing the need for capacity quotes on routes that were calmer just weeks ago.

"The US has breached the trade deal and Europe is ready to retaliate."

- Bernd Lange, European Parliament trade committee chair

Tariff Impact on Road Transport Europe: Sectors at Highest Risk

The first shock falls on steel and aluminium flows, where US-origin material becomes dramatically less competitive almost overnight. For carriers, that does not simply remove volume; it shifts procurement toward new mills and substitute origins, creating new customs routines on lanes into Germany, Poland, and the Czech Republic.

Agricultural and consumer goods are next. Refrigerated transport operators serving Belgian and Dutch ports may see US-origin food volumes replaced by South American and Australasian products, while customs teams handling motorcycles, bourbon, and textiles face more origin verification work during the first weeks of the tariff regime.

- Metals and industrial inputs demand immediate supplier re-routing because 50% US duties destroy price competitiveness.

- Food and temperature-controlled goods shift seasonally and geographically, which changes reefer demand around Belgian, Dutch, and Spanish gateways.

- Consumer goods with symbolic tariff exposure create heavy documentation work even when physical volumes are modest.

- Alternative-origin replenishment opens fresh road corridors through Turkey, Morocco, and other non-US supply points.

Before April 1, review HS codes, supplier origin declarations, and Incoterms together. One mismatch can turn a routine road handover into a clearance exception.

What the European Supply Chain Disruption Means for Carriers

For carriers, the challenge is a two-speed market. March demand is inflated by frontloading, but April could fragment into weaker US-origin imports, more customs-driven dwell, and stronger demand on alternative sourcing lanes.

That makes real-time tracking and accurate ETA control more important than usual. When tariff treatment can change by date, a late border handoff is not just a service problem; it can become a duty-cost problem.

+3%

Analysts expect average contracted European road freight prices to rise in 2026 even before additional tariff volatility is priced in.

Carriers also need a firmer view of fuel surcharge exposure as routes, wait times, and inland handling patterns change. Scenario planning with fuel cost models becomes essential when longer detours and customs queues start reshaping trip economics.

Longer-Term Effects: Modal Shifts, Nearshoring, and Corridor Rewrites

The dispute is also accelerating nearshoring logistics and multimodal testing. If transatlantic flows become less predictable, shippers will put more volume into shorter regional supply chains and use road transport as the connector between new suppliers, inland depots, and final production sites.

That does not eliminate road freight demand. Instead, it rewrites it into different corridors and denser customs nodes, especially where importers combine sea freight, bonded warehousing, and linehaul trucking to buffer against future tariff rounds.

Practical Action Plan Before April 1

The most effective response is a combined commercial and transport checklist. Teams that align procurement, customs, warehousing, and dispatch before the deadline will avoid the worst of the post-tariff scramble that typically follows a major policy switch.

- Audit every US-origin SKU against the Phase 1 and planned Phase 2 countermeasure lists before dispatching any late-March loads.

- Pull forward inbound loads that can still arrive before April 1 and confirm border timing with carriers, brokers, and receiving sites.

- Reserve bonded warehouse and overflow storage now because vacancy rates below 5% leave little room for delayed decision-making.

- Map alternative origin lanes for the top affected products and pre-brief carriers on customs document changes before demand spikes.

- Recheck public holiday calendars on key border routes using European holiday planning so the first tariff week does not collide with avoidable closure delays.

- Brief finance and operations together so duty exposure, spot-rate volatility, and service priorities are handled as one coordinated decision.

FAQ

How will EU retaliatory tariffs affect road freight rates?

The effect is mostly indirect but immediate. Tariffs change sourcing patterns, compress late-March export capacity, and push more freight through congested warehouses and customs nodes, which is why contract pricing already faces upward pressure even before every duty line is active.

What should European shippers do to prepare for trade war tariffs?

Start with a product-by-product customs review, then lock in warehousing, lane options, and carrier communication. The key is to decide before the deadline which loads must move now and which can tolerate higher post-April friction without damaging customer service or margins.

Which freight corridors in Europe are most affected by US tariffs?

The heaviest exposure sits on Hamburg, Rotterdam, Le Havre, and Barcelona-linked corridors because they connect manufacturing regions to export gateways and redistribution hubs. Those lanes see the sharpest combination of frontloading, storage scarcity, and customs-sensitive handoffs as the tariff regime changes.

Conclusion

The EU-US trade war is reshaping European road freight through timing pressure, not just through headline tariff percentages. Operators that secure capacity, storage, customs clarity, and updated market intelligence before April 1 will be far better positioned than those waiting for the political noise to settle.

Trade wars reloaded: Logistics in the crossfire of US tariff fallout

US has breached trade deal and Europe ready to retaliate: Bernd Lange

EU announces retaliatory tariffs in response to US tariffs on steel, aluminium and related products

The quiet before the trade storm: Tariff impact on Europe (EU) freight and imports

Tariff volatility pushes global supply chains into regional reset in 2026

How tariff shocks in 2026 are pushing firms toward regional supply networks