Strait of Hormuz Shutdown: What the Iran Conflict Means for Fuel Prices and European Road Freight

The Strait of Hormuz shock is lifting diesel costs across Europe. Learn how fuel volatility affects road freight quotes, surcharges and shipper planning.

Logifie Team

Logistics Technology Experts

From 28 February 2026 to 11 March 2026, attacks on ships, carrier suspensions and emergency oil-market measures turned the Strait of Hormuz into a pricing issue for European shippers. If you are tracking fuel prices across Europe , the reason is simple: diesel for road freight is priced in a global market, so a Gulf chokepoint can quickly change linehaul rates, surcharge tables and quote validity windows.

What happened in the Strait of Hormuz?

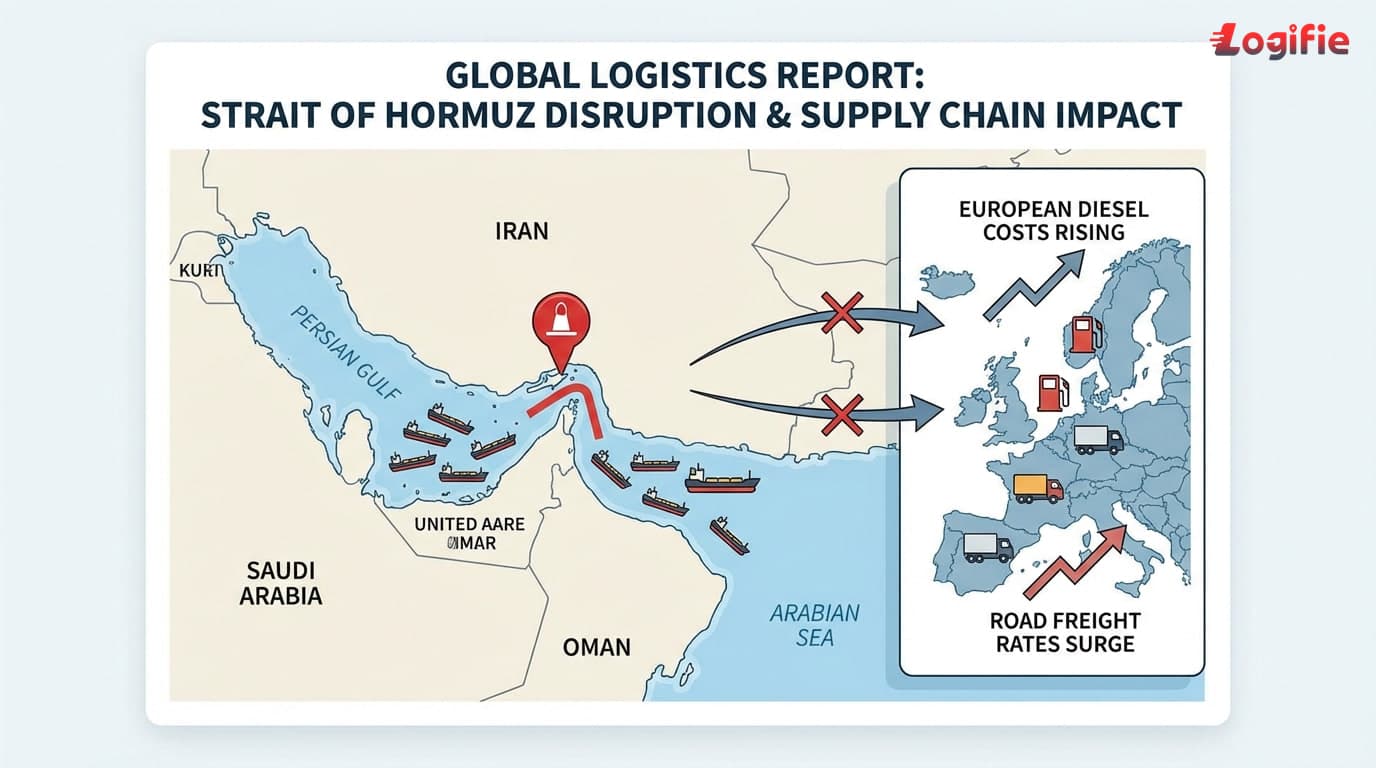

The Strait of Hormuz is a narrow route between the Persian Gulf and the Gulf of Oman, but its scale is global. The U.S. Energy Information Administration says 20.9 million barrels per day moved through the strait in 2023, or about one fifth of world petroleum liquids consumption. After the conflict escalated on 28 February 2026, attacks on ships and higher war-risk conditions made a core oil corridor look operationally unstable rather than routine.

That matters even before any government declares a formal legal closure. Once shipowners, insurers and carriers start avoiding the lane, the market behaves as if capacity has been closed. Hapag-Lloyd suspended Strait of Hormuz transits until further notice, and the result for buyers is slower energy flow, higher insurance costs and a larger risk premium inside diesel pricing.

Why diesel prices in Europe react even when Europe does not buy Iranian oil directly

Europe does not need to import Iranian crude directly for this to hurt. Diesel and crude are globally priced commodities, so any chokepoint that interrupts or delays Gulf exports changes the reference price paid by European refiners, distributors and hauliers. Reuters reported on 10 March 2026 that diesel markets were already upended because distillate supply was structurally tight, which is why diesel can rise faster than crude during this kind of event.

The early market data already show the pressure. The European Commission's Weekly Oil Bulletin put the EU average diesel price for the week of 2 March 2026 at about EUR 1.572 per litre, with meaningful differences between countries. That spread is exactly why buyers should watch current lane markets rather than rely on stale quarterly assumptions.

How the shock shows up on a road freight quote

Most buyers will see the Hormuz effect first in fuel clauses, surcharge tables and shorter validity periods, not in a dramatic line item called Middle East crisis. As explained in Logifie's fuel surcharges and tolls guide , fuel and toll mechanisms already move freight invoices up and down; a geopolitical diesel spike simply makes those formulas reprice faster.

The math becomes material very quickly. Using the 33.1 L/100 km long-haul baseline identified in the research, every EUR 0.10/L move in diesel adds about EUR 3.31 per 100 km to linehaul cost. On a 1,000 km lane, that is roughly EUR 33 before toll changes, buffer capacity or margin protection. In a volatile market, carriers respond by shortening quote validity, widening surcharge review windows and pushing for index-linked pricing instead of fixed monthly assumptions.

What shippers should do now

If current tenders or spot lanes are exposed, treat this as a procurement and planning issue, not just a news event. Use Logifie's Get Quote page when you need a fresh lane check, and align internally on which benchmark will trigger price adjustments.

- Shorten quote validity periods and avoid leaving crisis-affected lanes open on old assumptions for a full month.

- Index fuel clauses to a public benchmark such as the Weekly Oil Bulletin or a clearly defined national diesel reference.

- Watch surcharge stacking, because fuel can rise at the same time as toll, insurance and contingency costs.

- Secure capacity earlier on critical lanes instead of waiting for the week of loading.

- Monitor lane-level fuel pages and key corridor countries so procurement sees country dispersion, not just a single EU average.

Fuel is only one layer of the invoice. Policy-driven cost drivers described in Logifie's low-emission zones article and capacity constraints described in the EU cabotage rules guide can amplify the same shipment at the same time. Buyers should review the full cost stack together whenever diesel volatility spikes.

Which benchmarks to watch next

Three signals matter most over the next few weeks: the European Commission Weekly Oil Bulletin for published pump-price movement, EIA and IEA updates for global supply and emergency-stock policy, and carrier notices that show whether rerouting and war-risk behaviour are easing or hardening. The goal is not to predict headlines. The goal is to know when your contract assumptions no longer match the live market.

Also watch the policy buffer. The EU oil-stocks framework and the IEA's 11 March 2026 emergency release can soften a sustained shock, but they do not remove day-to-day volatility from trucking quotes. For freight buyers, strategic stocks are a stabiliser, not a reason to ignore current diesel pricing.

Conclusion

The Strait of Hormuz crisis matters to European road freight because diesel is global, distillates are tight, and freight contracts reprice faster when uncertainty rises. Buyers who benchmark fuel correctly, shorten quote validity and monitor lane-level cost signals will make better decisions than teams waiting for the monthly invoice surprise.

Sources

World Oil Transit Chokepoints (U.S. Energy Information Administration, 2024) - Explains that 20.9 million barrels per day moved through the Strait of Hormuz in 2023, roughly 20% of global petroleum liquids consumption, showing why disruptions at the chokepoint affect fuel pricing far beyond the Gulf.

How many ships have been attacked in the Gulf since the start of the Iran war? (Reuters, 2026) - Reports that multiple vessels were attacked in or near the Gulf after 28 February 2026, reinforcing the persistent risk environment that changed shipping and insurance behaviour.

Suspension of Strait of Hormuz transits due to security closure (Hapag-Lloyd, 2026) - Confirms that a major carrier suspended transits through the strait until further notice and warned customers about rerouting, schedule changes and delays.

Diesel markets upended by Middle East conflict threaten global economic slowdown (Reuters, 2026) - Explains that diesel supply losses and structurally tight distillate markets can push diesel prices higher and faster than crude, with Europe especially exposed.

EIA market-disruption release (U.S. Energy Information Administration, 2026) - States that Brent settled at USD 94 per barrel on 9 March 2026 after reduced shipments through the Strait of Hormuz, showing how the conflict kept a visible risk premium in the oil market.

IEA member countries to carry out largest ever oil stock release amid market disruptions from Middle East conflict (International Energy Agency, 2026) - Announces the 11 March 2026 coordinated emergency release of 400 million barrels, highlighting how governments tried to stabilise supply.

Weekly Oil Bulletin (European Commission, 2026) - Provides the Commission's official weekly fuel-price reporting view for EU member states, including the diesel benchmarks buyers can use to monitor short-term pricing changes.

Council Directive 2009/119/EC (EUR-Lex) - Sets the EU framework requiring member states to maintain emergency oil stocks equivalent to at least 90 days of net imports or 61 days of inland consumption, which explains the policy buffer behind market-stabilisation actions.